With the advent of the era of cloud computing, servers as the underlying infrastructure are also ushering in a huge market demand. Let's take a brief look at this industry today.

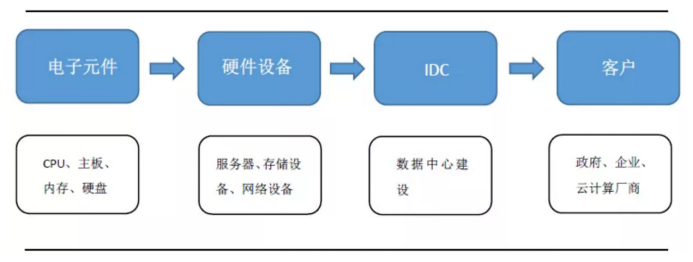

1. Industrial chain

2. Supply and demand analysis

2.1 Supply: determined by capacity, capacity utilization and inventory.

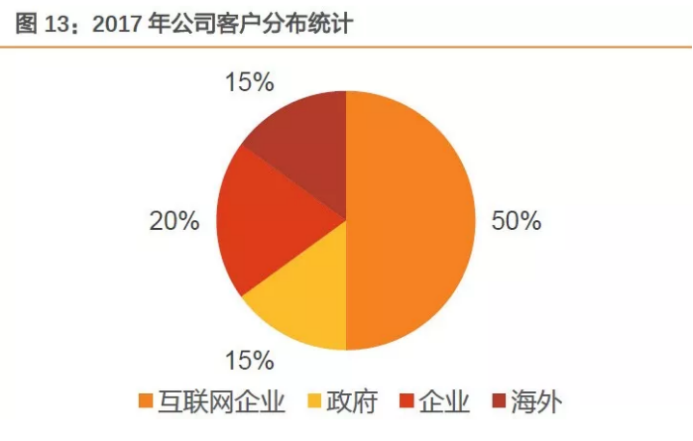

2.2 Demand: The downstream customers of server manufacturers can be mainly divided into cloud computing vendors, governments, and enterprises.

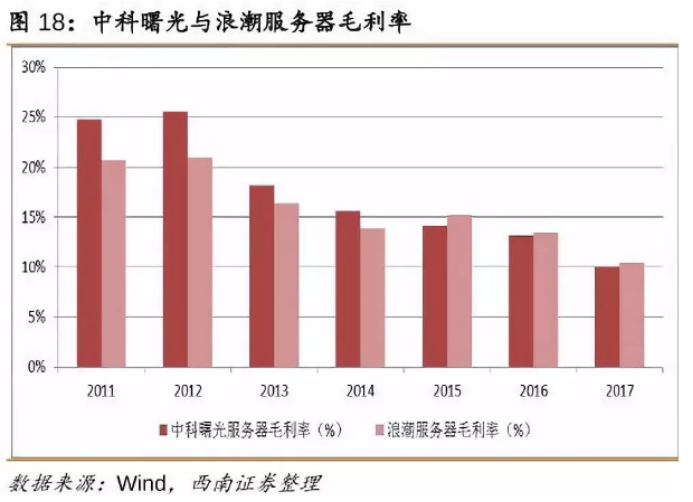

In Q1 2018, cloud server sales reached US$2.08 billion, a year-on-year increase of 126.5%, and contributed 51.7% to the growth of the overall market. The rapid growth and standardization of downstream Internet vendors' businesses, especially the rise of cloud computing service providers, has led to the further concentration of the original pattern of scattered customers, the bargaining power of server manufacturers, and the gross profit margin has continued to decline.

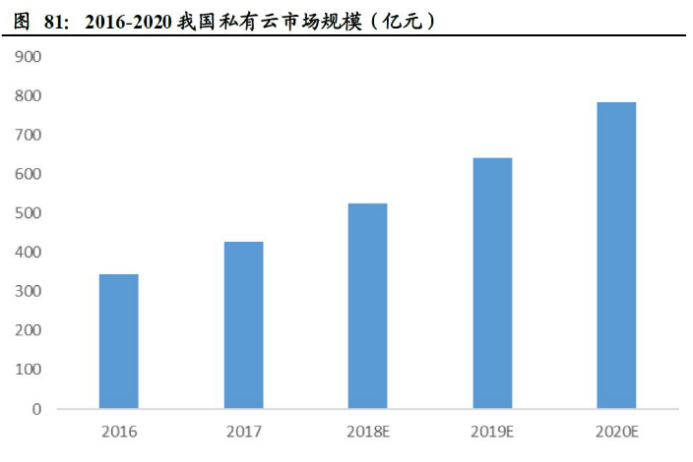

China's IT demand mainly from the government and telecommunications, banks and other state-owned capital-led enterprises, such departments to price sensitivity is relatively low, but the requirements for information security, service customization, etc. are extremely high, so at present China has deployed cloud computing enterprises in the proportion of private cloud is much higher than public cloud or hybrid cloud, considering that in the future China's cloud computing payment subject will still be the government / state-owned enterprises and other departments, it is expected that the construction of domestic private cloud will still develop at a relatively rapid pace. In 2017, the size of China's private cloud market was 42.7 billion yuan, and it will grow steadily in the future, reaching 78.4 billion yuan by 2020, with a CAGR of 22.75% from 2017 to 2020.

Demand Dynamics:

• The need for enterprises to reduce costs and improve efficiency: the gap between the degree of informatization of our enterprises and that of developed countries

• Government policy support

• The rapid development of the cloud computing industry

• The service requirements brought about by the application of artificial intelligence, especially the demand for deep learning servers

3. Profit analysis

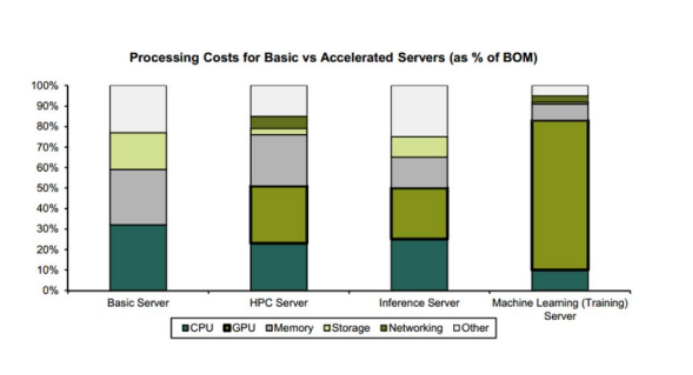

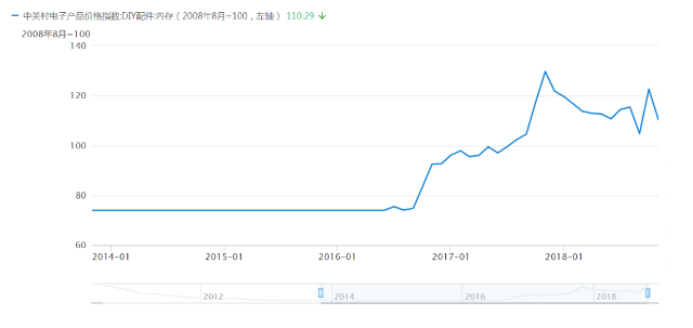

• Cost structure: The main components of server manufacturers include CPU, motherboard, memory, hard disk, etc., and the sharp fluctuation of upstream prices is closely related to the gross profit margin of server manufacturers.

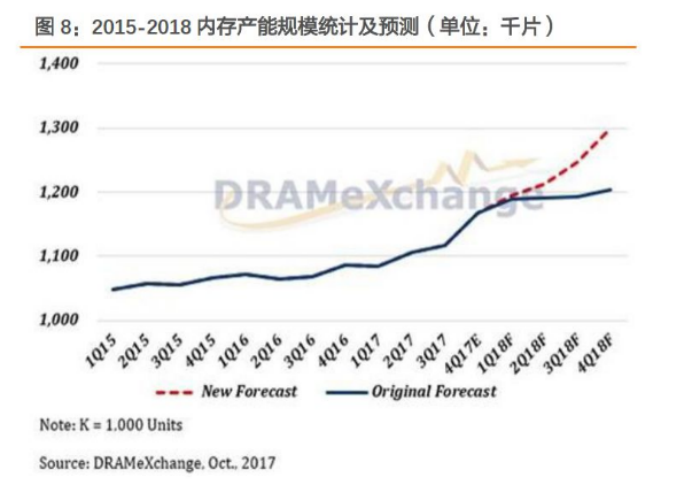

• Memory: The cost in the upstream market is relatively high, and the price mainly depends on the change of memory capacity and the fierce competition.

• Chips: China is highly dependent on foreign countries, and before 2017, Intel almost monopolized the field of x86 server chips (X86 chips accounted for 98% of global server sales in 2016), and its profit margin was as high as 49%, far exceeding the PC chip field (<30%). With the release of AMD's new data center processor EPYC series in 2017, it will change the market landscape of x86 commercial processors almost dominated by Intel.

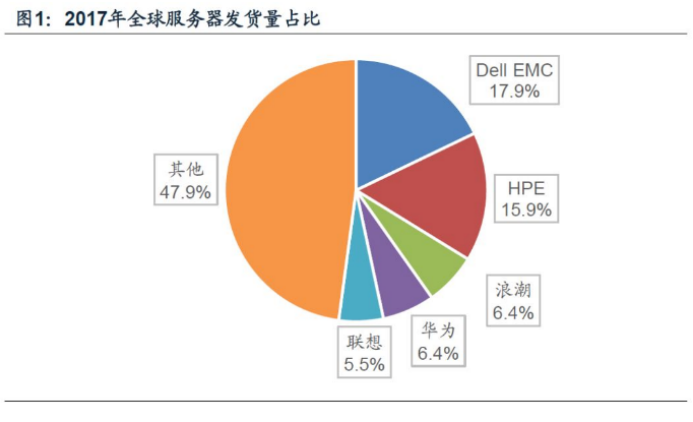

4. Competitive landscape

The industry is mainly made up of three types of businesses:

• Overseas brand server manufacturers: IBM, HP, DELL

• Local brand server manufacturers: Inspur, Lenovo

• White box server vendors

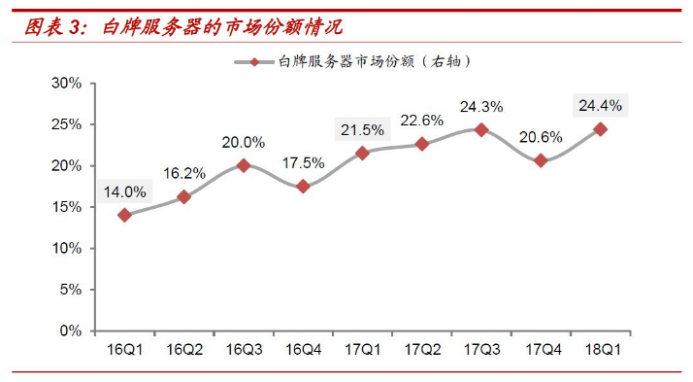

Local server manufacturers are far smaller than overseas competitors in terms of scale and R&D investment, and the gross profit margin level cannot be improved. Thanks to the advantages of "localization", local server manufacturers have greater advantages in government orders and other aspects. With the advent of the era of cloud computing, the demand point of cloud computing vendors for servers has changed, and at the same time, hardware open source has ushered in development opportunities for white-label machines, and the market share of white-label server manufacturers is steadily increasing.